.png)

The Four-Part Core R&D Qualification Checklist

For an activity to qualify for the tax credit, it must meet all four components of the IRS four-part test.

1. Qualified purpose (Section 174)

To begin, you must first determine if the cost of the activity was for a qualified purpose.

Check off the following statements:

- ☐ The work was completed as part of your trade or business.

- ☐ The activity represents research and development in the experimental or laboratory sense.

- ☐ The research efforts were intended to discover information that eliminates uncertainties concerning the improvement or development of a product.

- ☐ The activity wasn’t a routine inspection, quality control, or efficiency study.

- ☐ The activity wasn’t market research, promotional work, marketing, management studies, or similar non-technical tasks.

If you cannot check all these boxes, then the IRS will not consider the activity as qualified.

2. Technological information discovery

The next portion of the test determines if you researched to “discover information” for the purpose of reducing uncertainty. In plain English, uncertainty means you are trying to find out:

- If something will work,

- How to make it work, or

- What design will work best

Therefore, you must be able to check off the following:

- ☐ The purpose of the activity was to discover something technological, not just tweak aesthetics.

- ☐ The work relied on scientific or technical principles, such as engineering, biology, physics, or computer science.

- ☐ The work aimed to solve uncertainty about how to develop or improve a product or business component.

You get bonus points if your work is backed up with a US patent, since the IRS generally accepts this as proof of technological information discovery.

However, in many instances, patents are not granted until years after the fact, so alternative forms of proof will be required.

3. Business component

This test checks if the research was completed to create or improve something specific that the business will actually use or sell (rather than just general research).

If the work cannot be tied to a business component, then the IRS won’t consider it as qualified research:

- ☐ The research was intended to help develop new or improved business components (products, processes, software, techniques, inventions, etc.).

- ☐ Research can be directly linked to a specific business component.

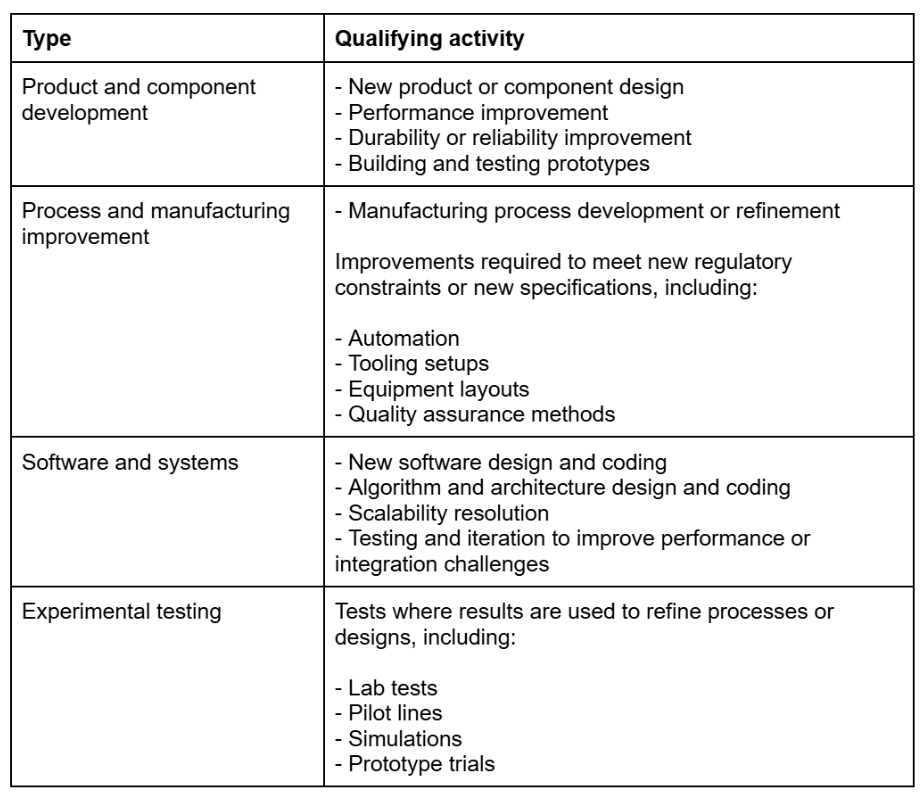

We’ve included a useful table further down this article to help you identify qualified activities and components.

4. Process of experimentation

The last section determines if real experimentation was carried out with documented trials, tests, or iterations.

To find out if the activity fits this criteria, you must check off all these boxes:

- ☐ There was uncertainty at the start, and you did not know what design or method would work.

- ☐ Different approaches were applied to resolve the uncertainty.

- ☐ Results were evaluated and iterated, and did not rely on one single method or guesswork.

- ☐ Experiments were carried out for a qualified purpose: Function, performance, reliability, and not simply for cosmetic changes.

A Deeper Look At Exclusions

Even if the activity satisfies all of the above criteria, it might still not count as qualified research. If the work involved any of the following exclusions, you can consider it disqualified:

- Research that was completed after commercial production, such as tooling or pilot runs

- Patents, models, production methods, and processes that were acquired from a third party

- Marketing, advertising, and promotions

- Activities performed outside the US and US territory

- Software intended for internal use only

- The duplication of existing products and processes from blueprints and plans

- Researching the existence of fossil fuels and minerals

- Expenditure for land and property

- Market research and consumer surveys

- Efficiency surveys

- Literary or historical research

- Management studies

- Routine testing and inspections

Examples of Qualifying Activities

To help you identify whether or not the activity qualifies, check to see if it matches an item on this list:

How to Prove the Qualifying Activity

Meeting all the criteria on the checklist is only part of the challenge. You must also prove who worked on what and when.

The IRS doesn’t just look at what qualifies; they need to see exactly how activities, time, and costs are tied to each qualifying component.

That means:

- Everything must be documented, including the problem that was being solved, the uncertainties, the hypotheses, and what tests and experiments were run.

- Costs, time spent on activities, and who worked on them must be tracked.

- All activities must link back to a specific business component.

Using time tracking software is a great solution because it keeps all records defensible and compliant with IRS expectations.

Time should be traceable from the employee to the activity and then to the business component, with clear connections at each step. Using time tracking software enables this level of detail with minimal effort from your team.

Here’s how:

Clear hierarchical work structures

Time tracking software allows you to arrange work into projects and tasks.

Each project can represent a specific business component. For example, an Inventory Forecasting Algorithm or a Customer Portal Performance Upgrade.

Tasks then capture the type of work that was completed within each project.

It’s important to make tasks specific and instantly identifiable. Therefore, avoid generic terms like “R&D,” “Miscellaneous,” etc.

Instead, use terms like:

- Technical design

- Testing and experimentation

- Data analysis

- Documentation of findings

Time tracking cadence

The IRS expects contemporaneous records of time spent on activities. Therefore, recording after the fact is a big no-no.

Users can utilize the start/stop timer in time tracking software to track R&D time in real-time, resulting in accurate and defensible timesheets.

For time tracking cadence best practice, users should:

- Log time daily, and as the activities occur.

- Log time in increments according to activity (start a new time entry every time the activity changes).

- Include precise details regarding the type of work carried out, what the results were, and the associated costs.

- Link time entries to proof of work (documentation).

We have comprehensive information available on what should go on an R&D time entry, so you can be sure that your workers create them correctly.

Use tags and custom fields as R&D qualifiers

Custom tags let you flag why the time qualifies, and they can also be used for things like separating qualified and non-qualified time and noting the activity phase.

Tags also make reviews faster and cleaner because they can be filtered in the reporting feature. That’s why they’re also used prominently for tracking CapEx and OpEx.

For instance, you might set up tags as follows:

- R&D: Experimentation

- R&D: Uncertainty

- R&D: Testing

- Non R&D: Support

- Non R&D: Production

Custom fields exist directly on projects, tasks, and time entries. You can use these to input supporting information, such as job codes, cost centers, or internal references used for payroll and accounting.

More importantly, custom fields can capture context that the IRS actually cares about, like the business component ID or name, or the type of uncertainty being addressed.

Used together, tags and customs fields allow you to separate classification from description. Tags quickly signal why time might qualify, while custom fields provide supporting detail for reviews and audits.

Documentation Required (Quick Checklist)

While the amount of documentation varies depending on the scope and size of the credit claim, some essentials must be included no matter what.

If this is your first year claiming the tax credit, expect to spend more time gathering documentation than you will in subsequent years.

This is because you must set up the various mechanisms (like time tracking) to ensure the right information is sufficiently captured.

Here’s a basic list of what you must provide:

- Nexus proof: You must provide a nexus between the qualified activities, the worker’s time, and their costs. The best way to do this is by using time tracking software.

- Four-part test qualification: You need documentation to demonstrate how each activity meets the four-part test. Documentation requirements vary by industry; you can use information generated during daily operations.

- Project and technical files: All the documentation associated with the activity. Project charters, design files, specs, test plans and results, change logs, and so on.

- Core tax forms: Form 6765 should be attached to the business income tax return.

- Payroll records and forms, including Form W-2 for workers engaged in R&D.

- Accounting records of costs and expenses used for R&D efforts.

- Contracts and statements of work carried out by third-party vendors.

- Any patent applications and invention disclosures.

- Relevant internal notes, like emails, meeting minutes, and status reports.

Final Thoughts

Claiming the R&D tax credit might seem complicated as it requires comprehensive workflows and document preparation.

However, with the right mechanisms in place, like time tracking software, the process will become easier, faster, and eventually a normal part of the working day.

You must also take time to train your staff in what’s expected of them. If they recognize and understand the importance of tracking qualified activities, they’ll be more willing to keep accurate time logs.